Consumer rewards credit card rates inch upward

April 30, 2012

Current averages:

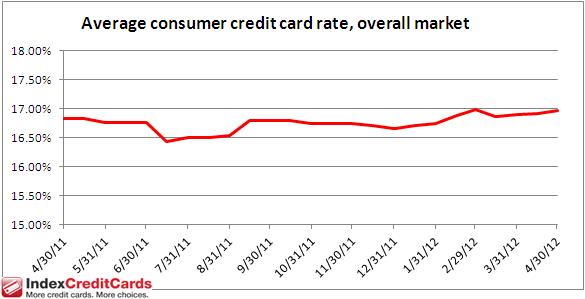

- Average consumer credit card rate, overall market: 16.97 percent

- Average consumer non-rewards credit card rate: 15.11 percent

- Average consumer rewards credit card rate: 17.76 percent

- Average student credit card rate: 16.98 percent

- Average business non-rewards credit card rte: 14.74 percent

- Average business rewards credit card rate: 15.40 percent

Once again the US bank prime rate was unchanged, at 3.25 percent.

Recent weeks have seen a series of discouraging economic reports. If this trend continues, it could affect credit card rates, though the nature of that impact may vary according to the applicant’s credit rating.

Economic slowdown could affect credit card rates

The month of April began with a disappointing employment report, as the net number of new jobs created in March dropped sharply from the prior month. April ended on an equally ominous note, as the last week of the month brought the news that durable goods orders had fallen by 4.2 percent during March, and that GDP had slowed to a 2.2 percent annual rate of real (inflation-adjusted) growth in the first quarter of 2012, down from a 3.0 percent growth rate in the fourth quarter of 2011.

If the economy is slowing, the reduced demand for credit could push some credit card rates downward, but the benefit would not be enjoyed equally by all credit card customers. Those with good credit would be most likely to see some reduction in their rates. However, a weakening economy could also raise credit quality concerns, so customers with shaky credit histories could see their rates rise as credit card companies adjust to a rising level of credit risk.

For now though, credit card offers changed only very slightly in the second half of April. It may be purely coincidental that one of the changes was a slight increase in the spread between rates for excellent-credit customers and those for weaker-credit customers. However, if the economy continues to worsen, that spread might keep getting wider.

Consumer credit cards

Consumer rewards credit card rates rose by 7 basis points in the second half of April, to 17.76 percent. Rates on consumer non-rewards credit cards were unchanged at 15.11 percent. As a result of the increase in rewards credit cards, the overall average for the consumer category rose by 5 basis points, to 16.97 percent.

This is the second consecutive survey which saw a widening in the difference in average rates for rewards and non-rewards credit cards. This is a reversal of a trend which had seen that difference become more narrow during the first 3 months of the year, though this spread is still much lower than it was at the end of 2011. Consumers can generally expect to pay higher interest rates in exchange for rewards programs, but the lower the difference in rates between rewards and non-rewards programs, the more attractive rewards programs become.

Student credit cards

The average rate on student credit cards remained at 16.98 percent, where it has been since the first half of March. This stability is especially valuable during the school year, when students may not have time to keep up with changes in their credit card terms.

Business credit cards

Rates for both categories of business credit cards were unchanged in the latter half of April. The average rate for business non-rewards credit cards remained at 14.74 percent while the average rate for business rewards programs stayed at 15.40 percent.

Business non-rewards credit cards have put together an impressive record of stability, as these rates have yet to change this year.

Good credit vs. average credit

Credit card offers for customers with strong credit histories are generally going to feature lower rates than those for customers with average or below-average credit. The rate advantage for having good credit increased slightly in the latest credit card survey, rising by 2 basis points to 4.24 percent.

In total, IndexCreditCards.com surveys information from some 50 different credit cards, and includes multiple credit-rating tiers from many of those cards. Examples of offers surveyed include American Express credit cards, Capital One, Chase, Citi, Discover, and other MasterCard and Visa branded cards. The information compiled not only demonstrates trends in credit card rates over time, but also indicates the different values credit card companies put on different target markets (consumer, business, etc.), as evidenced by the differences between rates for those markets.

Disclaimer:The information in this article is believed to be accurate as of the date it was written. Please keep in mind that credit card offers change frequently. Therefore, we cannot guarantee the accuracy of the information in this article. Reasonable efforts are made to maintain accurate information. See the online credit card application for full terms and conditions on offers and rewards. Please verify all terms and conditions of any credit card prior to applying.

This content is not provided by any company mentioned in this article. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any such company. CardRatings.com does not review every company or every offer available on the market.

Published