Credit card rates rise for bad credit applicants

January 15, 2012

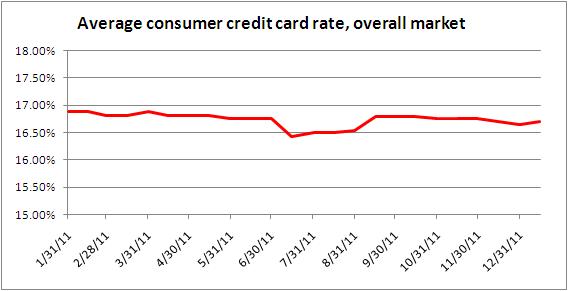

Current averages:

- Average consumer credit card rate, overall market: 16.70 percent

- Average consumer non-rewards credit card rate: 14.72 percent

- Average consumer rewards credit card rate: 17.55 percent

- Average student credit card rate: 17.06 percent

- Average business non-rewards credit card rate: 14.74 percent

- Average business rewards credit card rate: 15.53 percent

During the first half of January, the US bank prime rate remained unchanged at 3.25 percent.

While a change in the prime rate doesn’t seem to be on the horizon, there are other factors that can affect credit card rates, and concern over credit quality seemed to be a driving force behind the changes seen in the latest IndexCreditCards.com survey.

There were no changes in business or student credit cards this time around, but both the rewards and non-rewards categories of consumer cards increased in the first half of January 2012. These increases can be linked to the addition of a higher rate tier for weaker credit customers by one of the credit card companies in the survey.

This addition of a higher rate tier went hand-in-hand with a rise in the spread between credit card rates for applicants with good credit versus weak credit, suggesting that not all customers are experiencing the same trends. The cost of rising credit card rates in recent weeks is primarily being borne by people with lower credit ratings, while some customers with strong credit histories may actually have seen a decline in rates.

In short, while the general interest rate environment has been stable, credit card companies are evaluating safer and riskier credit customers as separate and distinct markets, and are making independent rate adjustments accordingly. In recent weeks, those evaluations and adjustments have favored customers with strong credit histories.

Consumer credit card rates

After reaching their lowest point for all of 2011 at the end of the year, consumer non-rewards credit card rates snapped back a bit in the early part of January, rising by 14 basis points (0.14 percent) to 14.72 percent. Consumer rewards credit card rates experienced a barely perceptible increase of just 1 basis point to 17.55 percent. Overall, consumer credit card rates rose by an average of 5 basis points to 16.70 percent.

It should be noted that rate increases were seen exclusively in the higher rate tiers of credit card offers, while there were actually some declines in the lower tiers. In short, whether or not a given consumer sees rates as rising or falling right now depends on that consumer’s credit history.

Student credit card rates

The average rate for student credit cards remained stable at 17.06 percent in the first half of January. This represents a welcome leveling off of student credit card rates, after they had risen in each of the two previous surveys for a total increase of 47 basis points.

Business credit card rates

Both non-rewards and rewards business credit cards were unchanged in the first half of January. Rates in both of these categories have been stable since late November.

Good credit vs. average credit

Perhaps the most distinct trend in credit card rates recently is the widening spread between rates for customers with good credit, and rates for those whose credit is average or worse. This spread widened to 4.07 percent in the most recent survey, after having been at 3.69 percent in late December, and 3.57 percent just before that. This raises an important point for anyone evaluating credit card offers. Credit card companies are likely to advertise their best rates, but customers that don’t have a strong credit history need to compare the rate tiers that are likely to apply to them.

In total, IndexCreditCards.com surveys information from some 50 different credit cards, and includes multiple credit-rating tiers from many of those cards. Examples of offers surveyed include American Express credit cards, Capital One, Chase, Citi, Discover, and other MasterCard and Visa branded cards. The information compiled not only demonstrates trends in credit card rates over time, but also indicates the different values credit card companies put on different target markets (consumer, business, etc.), as evidenced by the differences between rates for those markets.

Disclaimer:The information in this article is believed to be accurate as of the date it was written. Please keep in mind that credit card offers change frequently. Therefore, we cannot guarantee the accuracy of the information in this article. Reasonable efforts are made to maintain accurate information. See the online credit card application for full terms and conditions on offers and rewards. Please verify all terms and conditions of any credit card prior to applying.

This content is not provided by any company mentioned in this article. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any such company. CardRatings.com does not review every company or every offer available on the market.

Published