Business rewards credit cards buck rising trend

April 15, 2012

Current averages:

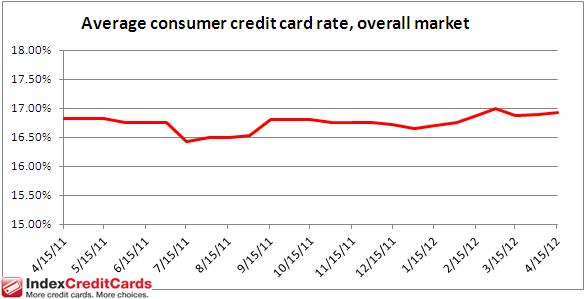

- Average consumer credit card rate, overall market: 16.92 percent

- Average consumer non-rewards credit card rate: 15.11 percent

- Average consumer rewards credit card rate: 17.69 percent

- Average student credit card rate: 16.98 percent

- Average business non-rewards credit card rate: 14.74 percent

- Average business rewards credit card rate: 15.40 percent

The US bank prime rate has been unchanged since the beginning of 2009, at 3.25 percent.

Contradictory trends

The first half of April saw contradictory trends in credit card offers. The movements in question occurred in the rewards categories of consumer and business credit cards: the average consumer rewards credit card rate rose slightly, while the average business rewards credit card rate fell. In turn, these changes affected the relationships between rewards and non-rewards cards, and between rates offered to customers with excellent credit ratings and those available to customers with average credit ratings.

Changes in these relationships will be discussed in more detail in the sections that follow, but as a general observation, these types of individual, segment-by-segment moves are what can be expected in an environment in which the bank prime rate has been unchanged for a long period of time.

The prime rate

If the prime rate were to change, one could expect credit card rates to move across all categories, and in the same direction. However, absent any across-the-board change in interest rates, credit card companies are left to assess the risk and attractiveness of each segment of the credit card market, and change rates only when one of those assessments changes.

This is why credit card rate changes over the past couple of years have tended to be somewhat piecemeal, occurring in one or two segments but not all of them. It also explains how some of the changes for different categories can appear to be contradictory, with one category of rates rising while another falls, as was the case this month.

Consumer credit cards

Consumer non-rewards credit card rates were unchanged at 15.11 percent, while the average rate on consumer rewards credit cards rose by 0.03 percent, to 17.69 percent. The overall consumer category average rose slightly as a result, to 16.92 percent.

The rise in consumer rewards credit card rates increased the gap between consumer rewards and non-rewards credit card rates, which is contrary to the prevailing trend so far this year. However, since the rise in consumer rewards credit card rates was so slight, it did little to reverse the changes this trend has brought overall. Currently, consumer rewards credit card rates are an average of 2.58 percent more expensive than their non-rewards counterparts. At the start of the year, this gap stood at 2.96 percent.

Student credit cards

The average interest rate on student credit cards was unchanged at 16.98 percent. This was the second consecutive credit card survey, spanning a month in time, for which rates in this category remained the same.

Business credit cards

Non-rewards rates for business credit cards held steady at 14.74 percent, while rates on business rewards credit cards dropped 13 points to 15.40 percent.

With rates on business rewards credit cards moving closer to those for non-rewards cards, early April saw the continuation of a trend which has been in place for the past several months. The spread in rates between these two categories has now reached its lowest level of the year at 0.66 percent. From a cost/benefit standpoint, this makes business rewards programs relatively more attractive than they have been all year.

Good credit vs. average credit

Since the rise in consumer rewards credit card rates occurred at one of the lowest rate tiers, this narrowed the spread between the best rates, which are available to customers with excellent credit, and average rates. For the latest survey, this spread dropped 4 points to 4.22 percent.

About the IndexCreditCards.com credit card rate monitor

In total, IndexCreditCards.com surveys information from some 50 different credit cards, and includes multiple credit-rating tiers from many of those cards. Examples of offers surveyed include American Express credit cards, Capital One, Chase, Citi, Discover, and other MasterCard and Visa branded cards. The information compiled not only demonstrates trends in credit card rates over time, but also indicates the different values credit card companies put on different target markets (consumer, business, etc.), as evidenced by the differences between rates for those markets.

Disclaimer:The information in this article is believed to be accurate as of the date it was written. Please keep in mind that credit card offers change frequently. Therefore, we cannot guarantee the accuracy of the information in this article. Reasonable efforts are made to maintain accurate information. See the online credit card application for full terms and conditions on offers and rewards. Please verify all terms and conditions of any credit card prior to applying.

This content is not provided by any company mentioned in this article. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any such company. CardRatings.com does not review every company or every offer available on the market.

Published