Credit card rates edge up for no-frills cards

March 31, 2012

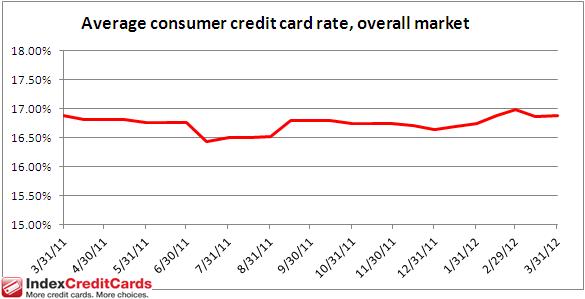

Current averages:

- Average consumer credit card rate, overall market: 16.89 percent

- Average consumer non-rewards credit card rate: 15.11 percent

- Average consumer rewards credit card rate: 17.66 percent

- Average student credit card rate: 16.98 percent

- Average business non-rewards credit card rate: 14.74 percent

- Average business rewards credit card rate: 15.53 percent

The US bank prime rate stayed at 3.25 percent, where it has been since the beginning of 2009.

Except for a slight rise in the average rate for consumer non-rewards credit cards, the second half of March was a quiet period for credit card offers. No other categories saw any changes.

Despite the calmness of credit card rates in recent weeks, there was a development in mid-March which could have important implications for credit card rates in the future. On March 16, the Bureau of Labor Statistics released its report on the Consumer Price Index (CPI) for February. This report showed that inflation, as measured by the CPI, increased by 0.4 percent in February.

If continued over the course of a full year, a 0.4 percent monthly rate of increase would result in annual inflation of nearly 5 percent. There’s not yet any reason to expect such a sharp rise in prices; one-month inflation readings are often volatile, and February’s surge follows four months of very quiet inflation numbers. Still, the inflation trend bears close monitoring, because the jump in February’s CPI was led by gasoline prices, which increased by 6 percent in a single month. Gasoline is not only an important component of the CPI, but it can also influence prices in other sectors as well.

This is significant for credit cards because lenders always keep a wary eye on inflation, and will raise interest rates if they feel it is necessary to protect themselves against rising prices. So far, it looks as though credit card companies are not going to over-react to one month’s inflation reading, but given recent limits on how and when they can raise credit card rates, they may not tolerate too much inflation before starting to act.

Consumer credit cards

Consumer non-rewards credit cards rose by 8 basis points, to 15.11 percent. Consumer rewards credit cards were unchanged at 17.66 percent. The average for consumer credit card rates overall rose by just 2 basis points, to 16.89 percent.

While the increase in non-rewards credit card rates was slight, it continued a trend which has been in evidence throughout 2012 so far, and that is a narrowing of the spread between consumer rewards and non-rewards credit card rates. With rewards credit card rates holding steady while non-rewards rates rose, this spread has now narrowed to 2.55 percent. It had been 2.96 percent when the year began, and 2.55 percent is as narrow as this spread has been since mid-August of last year.

The narrower this spread in rates gets, the more attractive rewards programs become, especially for customers who regularly carry a credit card balance.

Student credit cards

Student credit cards remained unchanged at 16.98 percent. This stability gives students an excellent opportunity to shop around and compare credit card rates, which is an exercise well worth doing. Even at the lowest rate tier, credit card offers for students range from a low of 11.99 percent to a high of 19.80 percent.

Business credit cards

Both categories of business credit cards were unchanged in late March. Business non-rewards credit card offers remained at an average of 14.74 percent, while business rewards credit cards remained at an average of 15.53 percent.

Good credit vs. average credit

With very little change in consumer credit card offers, the difference in rates for consumers with top credit ratings and those for consumers with average credit changed just slightly, widening by 3 basis points to 4.26 percent.

About the IndexCreditCards.com credit card rate monitor

In total, IndexCreditCards.com surveys information from some 50 different credit cards, and includes multiple credit-rating tiers from many of those cards. Examples of offers surveyed include American Express credit cards, Capital One, Chase, Citi, Discover, and other MasterCard and Visa branded cards. The information compiled not only demonstrates trends in credit card rates over time, but also indicates the different values credit card companies put on different target markets (consumer, business, etc.), as evidenced by the differences between rates for those markets.

Disclaimer:The information in this article is believed to be accurate as of the date it was written. Please keep in mind that credit card offers change frequently. Therefore, we cannot guarantee the accuracy of the information in this article. Reasonable efforts are made to maintain accurate information. See the online credit card application for full terms and conditions on offers and rewards. Please verify all terms and conditions of any credit card prior to applying.

This content is not provided by any company mentioned in this article. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any such company. CardRatings.com does not review every company or every offer available on the market.

Published